The special needs community faced a cruel financial paradox for decades….

To qualify for essential benefits like SSI and Medicaid, individuals were forced to remain in a state of “perpetual poverty”.

The “asset limit” of $2,000 meant that saving for a rainy day, a future home, or even a reliable vehicle was effectively illegal!

Not any more…

The ABLE Act (Achieving a Better Life Experience) of 2014 changed that narrative forever.

We talked about the history of the ABLE account in a previous article and also explored the funding best practices in our last article.

By allowing eligible individuals to save up to $100,000 (for SSI recipients) or more (for Medicaid-only recipients) in a tax-advantaged account, the law replaced the “spend-down” mentality with a “save-up” strategy.

Yea!!! 😊

However, opening the account is only the first step.

But 1st, a word from the legal team……. 😊

Disclaimer: All information provided in this article is strictly for educational purposes and is in no way deemed to be financial, tax, or legal advice. Please always consult with a qualified tax professional or attorney before making financial decisions, as laws and regulations can change. External links are provided for convenience and informational purposes only; they do not constitute endorsement or approval by Special Need Finances of any of the products, services or opinions of the corporation or organization or individual. Special Need Finances bears no responsibility for the accuracy, legality or content of the external site or for that of subsequent links.

To truly leverage this tool, you need a sophisticated funding strategy.

In this guide, we answer the most critical questions you need answers for such as:

- What are the funding source options, funding strategies, and key considerations for funding an ABLE account?

- What are the key questions to ask to determine the best funding strategy?

- Who are the eligible people (support circle) that can fund an ABLE account?

- What are the key considerations for choosing a funding strategy?

- Which funding options have the best tax advantages for both parents and recipients?

- What is the grandparent provision for funding an ABLE account?

Who Can Fund an ABLE Account?

One of the most powerful features of the ABLE account is that the beneficiary does not have to be the sole contributor.

The law recognizes that it takes a village to support an individual with special needs.

That is why the ABLE Act of 2014 allows for a “Circle of Support” to work together to collectively build the account’s value WITHOUT triggering the “gift-as-income” rules that plagued SSI recipients in the past.

Eligible contributors include:

- The Beneficiary: The individual with special needs.

- Parents and Guardians: The most common and primary funders of this funding strategy.

- Grandparents: Often the source of larger, long-term gifts.

- Extended Family and Friends: Aunts, uncles, cousins, and family friends who want to contribute to the child’s future.

- Employers: A growing number of employers are now offering ABLE contributions as a “disability inclusive” benefit AND alternative to 401k matching.

- Trusts: A Special Needs Trusts (SNT) can distribute or “pour over” funds into an ABLE account to replenish funds and to provide the beneficiary with a more direct cash access via a debit card.

- Organizations: Non-profits or community groups can contribute to an individual’s ABLE account as part of a scholarship or grant.

Defining Your Funding Source Options

Understanding where the money comes from is essential for tax planning and benefit protection.

There are five primary ways to move money into an ABLE account:

Personal Income and Savings

The beneficiary can deposit their own earnings from a job or social security payments.

This is the simplest form of funding and promotes financial responsibility, personal dignity, and financial autonomy.

Here is an example….

Sarah works part-time at a local library.

Previously, she had to spend her entire paycheck every month to stay under the $2,000 total resource limit required to maintain her SSI eligibility.

Now, she directs $300 from every paycheck into her ABLE account in order to save for a future apartment.

… Love it!!! 😊

The ABLE to Work Act

This is a gamechanger for employed beneficiaries.

If the account owner is working and does not participate in an employer-sponsored retirement plan (e.g. 401k), they can contribute additional funds beyond the standard annual limit.

- Standard Limit (2024): $20,000 in 2026

- ABLE to Work Additional Contribution: Up to the lesser of the beneficiary’s compensation for the year or the federal poverty line for 1-person household (approx. $15,560 in 2026).

- The Math: This means that a beneficiary could potentially deposit over $35,000 into their ABLE account in 2026 ($20,000 standard contribution limit + $15,650 ABLE To Work provision limit)!!!!

Family and Friends (The Circle of Support)

Contributions can be one-time or recurring.

Many state ABLE plans now offer “gifting platforms.”

These are secure, personalized links that a family can share with their network to enable the beneficiary’s “circle of support” to contribute funds to their ABLE account.

Here’s an example…

Instead of a GoFundMe, which can count as “countable income” and jeopardize the beneficiary’s benefits, a family shares an ABLE gift link.

Friends can contribute directly to the account and the money is never “seen” by the Social Security Administration as income to the beneficiary.

This is all legal and legit!

GOD, I LOVE legal loopholes!!! Lol 😊

Gifts and Special Events

Instead of traditional toys or clothes that may clutter a home, families can encourage “ABLE gifts” for birthdays, graduations, or holidays.

This turns a fleeting gift into a long-term investment.

Here is an example…

For a 1st birthday, a family asks guests to contribute to the child’s ABLE account instead of buying toys.

This early start allows for nearly two decades of compound growth before the child reaches adulthood!

Let’s face it, toys are nice and appreciated by the child BUT don’t last long since either the toy breaks or the child grows tired of it in a couple of years.

BUT a monetary gift to an ABLE account can literally benefit them for DECADES!

Not a bad option, huh?

Account Transfers and Rollovers

You can move funds from other savings vehicles into an ABLE Account:

- 529-to-ABLE Rollover (Most Common): If a child has a traditional 529 college savings plan but if their circumstances make higher education unlikely or their path needs to change, the family can roll those funds into an ABLE account (up to the annual limit) without taxes or penalties.

- UTMA/UGMA Transfers: Funds in “Uniform Transfers to Minors” accounts are often considered the child’s asset and can disqualify them from SSI at age 18. These funds can be moved into an ABLE account to “shield” them from the asset limit BUT it can require careful legal oversight.

Key Questions to Determine Your Best Funding Strategy

Before you make your first deposit, ask these six questions to ensure your strategy aligns with your specific life circumstances:

What are my short-term vs. long-term financial goals?

Are you saving for a new wheelchair next year (short-term) or a down payment on a condo in 10 years (long-term)?

This dictates whether you choose conservative or aggressive investment options.

Strategy:

Short-term goals should be kept in the “Cash” or “FDIC-insured” option of the ABLE plan.

Long-term goals should be invested in the plan’s equity or bond portfolios to fight inflation.

What is the minimum contribution needed to open the account?

Most plans require as little as $25 to $50 to get started.

How much and how often can I afford to deposit?

Automation is the key to success.

Setting up an automated monthly transfer of even $50 can create a substantial safety net over time.

Strategy:

Set up a consistent, automated monthly transfer of as little as $50 (more if you can).

This starts the creation of a consistent safety net and ensures the account remains active.

Does my state offer specific perks?

Some states provide state income tax deductions or credit for contributions.

More importantly, some states have passed laws exempting their state’s plan from “Medicaid Payback”.

What is the “Medicaid Payback” Rule?

This is a federal law that allows Medicaid to “claw back” remaining funds in an ABLE account after a beneficiary passes away to recoup costs.

While federal law mandates recovery for certain services, states have flexibility in defining “undue hardship” and estate definitions that make it exempt in their state.

Common Exemptions and “Hardship” Scenarios

All states are required to allow exemptions based on “undue hardship”.

You can request a waiver if recovery would cause such hardship.

Common exemptions include:

- Surviving Spouse: States cannot recover if a beneficiary is survived by a spouse.

- Disabled/Minor Children: Exemption for children under 21 or blind/disabled children of any age.

- Sibling Caretaker: A sibling with an equity interest who was living in the home for at least one year before the recipient’s institutionalization.

- Adult Child Caretaker: A child who resided in the home and provided care that delayed the parent’s nursing home placement.

- Hardship Waiver: The heirs would become eligible for public assistance if forced to pay the claim.

Finding a state that has laws exempting their state’s plan means the state Will Not claim the remaining funds after the beneficiary passes away.

Check to see if your state is one of these.

For example:

States like Pennsylvania and Maryland have passed laws stating they will not pursue this payback for their state residents using their state plan.

Check State-Specific Resources

- State Medicaid Agency: Search for “[Your State] Medicaid Estate Recovery Program” or “[Your State] Department of Health and Human Services.” They must, by federal law, inform applicants about recovery.

- Estate Recovery FAQ/Manuals: Many states publish “Frequently Asked Questions” documents or policy manuals online that explicitly list exemptions, such as those in Michigan.

- Triage Cancer Estate Recovery Tool: Triage Cancer provides a state-by-state breakdown of Medicaid estate recovery laws, including links to specific state exemptions.

- KFF (Kaiser Family Foundation): KFF publishes reports on state variations in Medicaid estate recovery, including data on which states waive recovery for homes of modest value

What are the fees?

Check the annual maintenance fees and the costs for using debit cards or checks.

High fees can eat into small accounts quickly.

If you plan to use the account for daily spending, look for a plan with a low-fee debit card.

How much can others contribute?

Ensure you don’t accidentally exceed the annual limit ($20,000 in 2026) by coordinating with grandparents and friends.

Coordination is vital.

If Grandma puts in $12,000 and the parents put in $12,000, you have exceeded the $20,000 annual limit for 2026CY which can lead to tax penalties.

The “Grandparent Provision” and Tax Advantages

When it comes to taxes, ABLE accounts offer a “double win” for parents and recipients.

For the Recipient:

All growth in the account is federal tax-free.

When you withdraw money for Qualified Disability Expenses (QDEs), which include nearly everything from rent and groceries to health insurance and transportation, you pay ZERO taxes on the earnings.

For the Parents and Grandparents:

Some states allow a state income tax deduction or credit for contributions made to an ABLE plan.

The Grandparent Provision

- Estate Planning: While not a formal “legal” term in the tax code, the “Grandparent Provision” refers to the Estate Planning: Grandparents can contribute up to the annual limit ($20,000) without triggering a gift tax or needing to file a gift tax return. This effectively moves money out of the grandparents’ taxable estate and into a protected vehicle for the grandchild.

- The 529 Loophole: If a grandparent has overfunded a 529 college savings plan for a grandchild who is ABLE-eligible, they can roll those funds into the ABLE account. This is a tax-efficient way to repurpose family wealth for the child’s care without the grandparent having to take a non-qualified withdrawal and pay a 10% penalty.

Key Practical Financial Considerations When Choosing an ABLE Plan

Not all ABLE plans are created equally AND you are NOT required to choose your state’s plan.

When selecting a plan, you can choose any state’s plan that is open to national residents.

Consider these features when selecting the plan that is right for your needs:

- Banking Functionality: Does the plan offer an FDIC-insured savings option? Does it come with a debit card or a checking account? For many beneficiaries, having a debit card is the first time they have experienced true financial independence.

- Withdrawal Limits: Are there limits on how many times you can move money per month? Some plans treat the account as a high-yield savings account with limited transfers. If using this as a “spending account”, you’ll need a plan with high liquidity.

- Gifting Platforms: Does the plan have a user-friendly way for friends to contribute? A simple link can make a huge difference during graduation or birthday season.

- National vs. State Program: If you live in a state with a great tax deduction (e.g. Maryland, Pennsylvania, Indiana, etc.), you should likely stay in-state. If your state has no tax deduction, look for “National Programs” with the lowest fees and best investment options (e.g. Ohio’s STABLE account or the Nebraska plan) which has very low fees and good investment options.

How To Pick the Best ABLE Account Investment Strategy

The short answer is …. know thyself!

To break it down further, you need to know the following to pick the best ABLE account investment strategy that also makes you feel the most comfortable investing money on their behalf:

- The purpose (goals) of the ABLE account

- The investing time horizon (e.g. how much time before your special needs loved one needs to use the money and how long the funds will need to last them).

- Your personal risk tolerance for investing money on their behalf

The purpose (goal) of the ABLE account is very important in determining the usage of the ABLE account.

For example, is the primary purpose (goal) of the ABLE account for saving for post-secondary education? Daily living expenses? Paying their medical bills? Buying a car? All of the above and more?

Here are examples of different goals and their generic timelines:

- Short-term goals – saving for their daily living expenses or car purchase in the next 1-5 years

- Medium-term goals – saving for a child’s college tuition expenses coming up in 5-15 years

- Long-term goals – saving for your child’s retirement, home purchase, and/or other long-term needs that could be 15 or more years away

Which leads to the next 2 points since they are related: investing time horizon and your own personal risk tolerance.

The time horizon of each goal will help determine what kinds of investments will be most appropriate for trying to reach that goal without putting too much of the principal at risk.

You have to be much more careful with money that you may need sooner, as a loss may force you to put off, reconsider, or cancel a goal altogether.

Remember, you are investing for them NOT yourself BUT you also have to be comfortable with the amount of risk chosen so YOU can sleep at night too! 😊

Here is where it gets tricky when assessing risk tolerance: you need to think of their needs BUT your level of risk tolerance!

This is because you are planning for your child’s future on their behalf.

Odds on, they won’t be investing the money so you need to make sure that whatever you do, you don’t lose sleep over your investing choices.

If struggling to understand your personal level of risk tolerance, I found a couple of awesome questionnaires to help you:

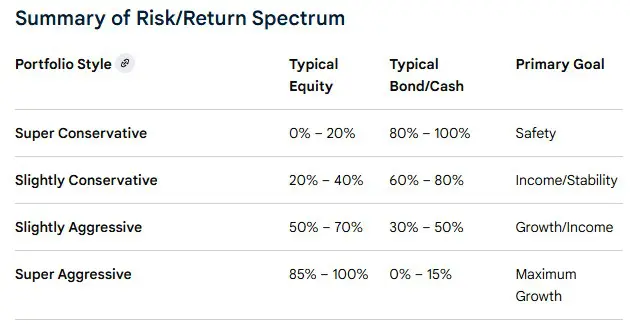

Once you understand your risk tolerance, here are some generic guidelines for each risk category type and generic investment selections.

Super Conservative (Capital Preservation)

- Objective: Maximize security and protect capital from loss. Minimal risk of volatility is preferred over higher returns.

- Allocation: Roughly 0%–20% stocks, 60%–80% bonds, and 20%–40% cash equivalents.

- Target: Investors in late retirement or those with a very short-term need for the funds (e.g., within 1–2 years).

- What to expect: Very low fluctuations, returns that may barely keep up with inflation.

Slightly Conservative (Conservative Growth)

- Objective: Prioritize capital preservation while seeking some income and modest growth to hedge against inflation.

- Allocation: Roughly 20%–40% stocks and 60%–80% fixed income (bonds/cash).

- Target: Conservative investors who can tolerate minimal market fluctuations.

- What to expect: Steady, modest returns with low-to-moderate volatility.

Slightly Aggressive (Growth & Income)

- Objective: Balance income generation with capital appreciation. Seeks growth but is willing to accept some downturns.

- Allocation: Roughly 50%–70% stocks and 30%–50% bonds.

- Target: Moderate investors with a 5+ year time horizon who can handle moderate, temporary losses for higher long-term gains.

- What to expect: Balanced portfolio performance – growing in bull markets and experiencing moderate decline in bear markets.

Super Aggressive (Maximum Growth)

- Objective: Maximize long-term capital appreciation. High volatility is expected and accepted to achieve maximum returns.

- Allocation: Roughly 85%–100% stocks, with 0%–15% in fixed income. Often includes international stocks and high-growth sectors.

- Target: Younger investors with a long-time horizon (15+ years) who do not need the money soon and can weather significant market drops.

- What to expect: A “roller coaster” effect—high gains, but also potential for significant short-term losses.

Conclusion: Building a Sustainable Future

The ABLE account is the most significant financial advancement for special needs families in a generation.

It effectively ends the era of forced poverty and gives individuals with special needs the ability to save for their own dreams WITHOUT impacting their SSI or Medicaid benefits.

However, the account is only as good as the strategy behind it.

By identifying your “Circle of Support,” maximizing the “ABLE to Work” provisions, and choosing a plan with the right banking features, you can turn a simple savings account into a lifetime of independence.

Don’t let the complexity of the tax code stop you.

Start small, ask the right questions, and begin building that safety net today.

Ready to take the next step?

Sign up for our newsletter and stay updated on the latest changes to the special needs tax code.

If you need help…… Zeke and I are glad to assist!

We have the knowledge, products, and services to help you level up your financial game!

OR

if you need more specialized 1 on 1 support…

I highly recommend consulting with a financial advisor who specializes in special needs planning to explore your options… Like Zeke! 😊

Schedule a call with my friend Zeke Zimmerman here!

Live The Life You Love, Want, And Deserve! 😊